This post may contain affiliate links. Full disclosure policy

After a bit of a hiatus, I’m delighted to welcome back my friend Peggy Doviak, fierce and fabulous financial guru and author of 52 Weeks to Prosperity, and turn today’s blog over to her. Peggy’s wise and timely advice on financing education is loaded with tips on how to pay for school without loading up on debt

Can you believe how quickly the summer ending? It seems like just last week, my family and I were watching 4th of July fireworks, and making homemade ice cream! Now, back to school activities are top priority in everyone’s mind.

In my hometown of Norman, OK, heading back to school reminds us that University of Oklahoma football is just around the corner. In Oklahoma, football is the most wonderful time of the year–Boomer Sooner!

However, if you aren’t a star quarterback on scholarship, college can be insanely expensive. Trying to figure out how to fund a college education can make you feel like you’ve been tackled. Here are a few defensive moves.

Getting Money Elsewhere

First, scholarships and grants can help lower the burden of paying for college. Look for individual characteristics, talents, and interests that might help you qualify for assistance. Remember, too, that good grades in high school may be worth more money than a minimum wage job in a fast food restaurant. All teenagers need spending money, and we want them to learn responsibility. However, short-term earned cash might not be as valuable as time to study. Additionally, participating in school activities could lead to scholarships, and if your child is working, there might not be time.

Further, because many scholarships are based on college entrance exams, have your child take exam review classes and practice tests to help raise his or her score. Unfortunately, college entrance has become something of a contact sport, so scoring very well on these exams is more important than ever.

Additionally, you can save money and help your teen bridge between high school and a large university by having them take freshman classes at community colleges. Just be careful that these courses don’t lower the chance your teen might be accepted at a prestigious university if that’s a goal. On the other hand, if your child enrolls in high school and the community college concurrently, acceptance chances may improve.

“Toto, I Don’t Think We’re In Kansas Anymore”

Another strategy for lowering expenses is by paying in-state tuition rather than out of state. If your teen is going away to college, research if it’s possible to establish residency in the new state. Although it might take a couple of years, the savings could be significant. Remember that if your child is no longer your dependent, they likely can no longer provide you with tax advantages; however, changes in the new tax laws have eliminated exemptions for dependents on your tax return. A more pressing concern could be losing the ability to carry your son or daughter on your insurance.

Start Saving Early

One of the easiest ways to cover college costs is through saving money when your children are younger. Several strategies can provide you with tax savings for doing this. For example, your state’s 529 qualified tuition plan provides tax-free investment growth when the funds are used for qualified post-secondary education expenses. The definition of “qualified expenses” is very broad and often can be useful even for students on scholarship. Additionally, you may receive a tax savings if you enroll in your state’s plan and you pay state income tax. Recent tax reform allows some of the funds to be used to pay for elementary and secondary private school tuition, although that usage is more limited.

Be careful about enrolling in out-of-state 529 plans. Sometimes, financial advisers claim they are better. You should know it’s likely that the adviser is receiving a commission or other compensation if you choose their recommended plan. Although sometimes your state’s option may not be the best choice for you, I believe most of the time, it’s fine. Rather than paying an adviser, consider enrolling your child in your state’s plan, yourself. Research the fund choices carefully to choose an appropriate risk tolerance level, keeping in mind how long it will be before your child needs to access the money.

What About Education Before College?

A second college funding vehicle is the Coverdell Education Savings Account (ESA). ESAs have a much lower annual contribution limit ($2,000) and an income phaseout level ($220,000 if married, less with other tax filing statuses). However, ESAs have a useful feature not found in 529 plans. The funds can be used for any school-approved expenses in primary and secondary education.

In English, this means it can pay for band instruments, football helmets, even internet access—for children not yet in college. As long as the expense is for a school-sponsored event, the account funds can be used. Coverdell ESAs are funded in after tax dollars, and the growth is not taxed when used for educational costs. If you qualify, funding a Coverdell could be a great option for very young children. Their youth will give the account time to grow and their education plans are not yet set. Any unused funds can be rolled into a 529 plan.

You have many different strategies for funding education expenses. Starting early and being creative will make you most successful. But, as a word of warning, don’t fund your children’s education at the expense of your own retirement savings. This mindset can cause your retirement to be underfunded—an event with disastrous results. No one wants to imagine depending on their children for support when they are elderly, but it happens remarkably often. Last, don’t be distressed if you can’t provide financial support. Remember that every good team has cheerleaders and unwavering fans. Emotional support may prove to be more valuable to your children than money.

Do you love Peggy and want to read more? Check out previous posts she’s written: Prosperity is about so much more than money, Setting and achieving financial goals, The Fierce way to curb spending, and When Can I Retire?

Meet Peggy

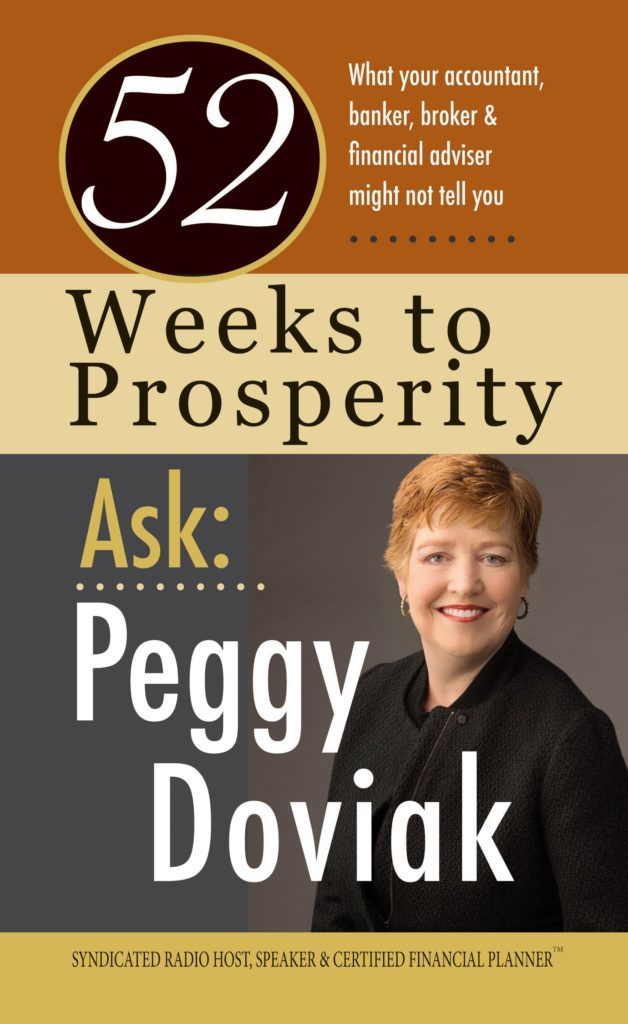

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.