This post may contain affiliate links. Full disclosure policy

I’m thrilled to welcome back my fierce friend, Peggy Doviak, to share her wisdom on end of year financial planning tasks to set us up for success next year.

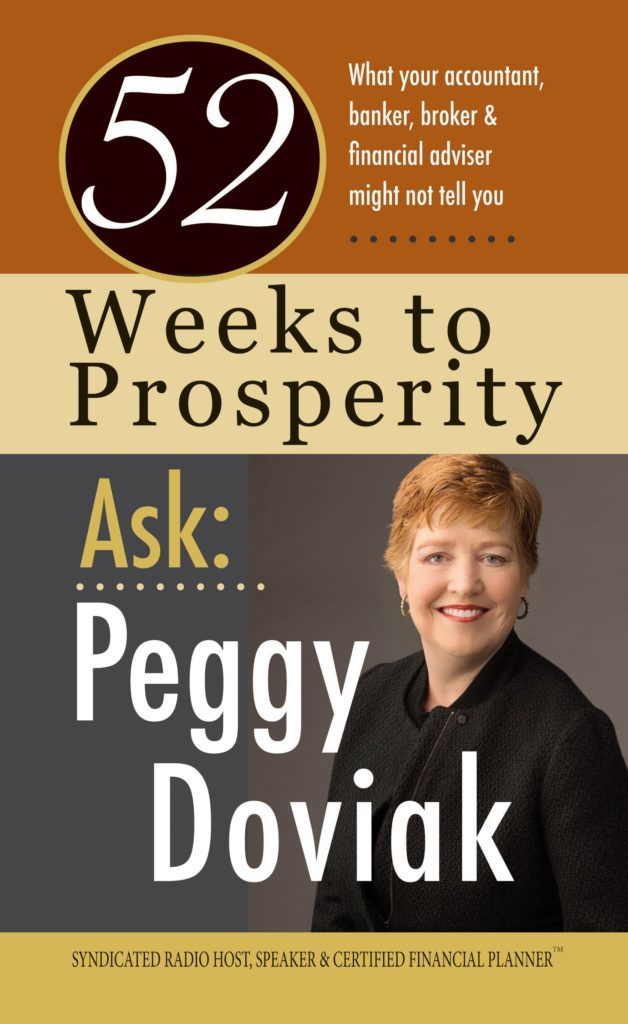

Peggy is the author of 52 Weeks to Prosperity along with other blogs posts you can find on Fierce Beyond 50 like: paying for college, advice about prosperity vs. money, setting financial goals, saving for retirement and curbing your holiday spending. She has a wealth of advice and we’re all better served by having a professional like Peggy in our corner!

Your Financial Planning Checklist for the End of the Year

It seems incredible that the holiday season is less than a month away! Once we reach Thanksgiving, free time vanishes until January. But right now, the back-to-school rush has passed, and we still have a little time before we defrost the turkey. Take advantage of the lull and finish up some important end-of-year financial planning tasks.

Step 1: Requirement Minimum Distributions

First, don’t forget to take your 2019 required minimum distributions, also called RMDs. If you are 70 ½ and have a traditional Individual Retirement Account, you must begin to take mandatory withdrawals. Up until now, the IRS has allowed you to defer taxes on at least the investment growth and possibly the money used to fund the account. Now, it’s time to begin to pay the tax liability. Fortunately, your required withdrawal is likely not as much as you expect. However, if you don’t follow the rules, you will pay a penalty of 50% of the amount you were supposed to take. That’s an expensive mistake!

If you want to postpone paying your taxes just a little longer, the IRS gives you a one-time option of deferring your first distribution until April 1st of the next year. Just remember you will also need to take a second withdrawal before December 31st as well. Unfortunately, there are a few more wrinkles. If you have a Roth IRA, you don’t need to take RMDs during your lifetime. Further, if you are still working after age 70 ½, you don’t have to take a distribution on a 401(k), 403(b), or other qualified account until you retire. This exception assumes you aren’t the business owner. However, postponing your distribution isn’t possible if you own a SEP or SIMPLE plan. Because these are based on IRAs, you must take distributions at 70 ½ even if you are still working.

Lastly, if you inherit an IRA, you also must take required minimum distributions. These begin by December 31stof the year after the year the person died. The delay allows most estate issues to be settled before money must be withdrawn. The RMD calculation of an inherited IRA is a little different than if the account had been your own. I recommend talking to a CPA or CERTIFIED FINANCIAL PLANNERTMpractitioner to help with this computation as well as all the other details around your required minimum distributions.

Step 2: Max Out Those Tax Deductions

Next, let’s move on to maximizing your tax deductions before the end of the year. Begin by looking at your charitable contributions. The Tax Cuts and Jobs Act didn’t actually eliminate your ability to deduct donations. However, the amount of the standard deduction is now so high that most people can’t exceed it. Still, check your records. If you can itemize your deductions in 2019, it might make sense to donate extra to charity this year if you anticipate not being able to itemize next year. That way, you receive a maximum tax benefit, and you help the causes you love.

Step 3: Take a Look at your Medical Expenses

You should also review your medical expenses. Remember that to be deductible, your bills need to be higher than 10% of your adjusted gross income, up from last year’s 7.5%. If you’re close to the deductible level, you might consider requesting appointments or paying extra medical costs, like new glasses or hearing aids, this year.

Step 4: Fund that 401k

Finally, although you can fund an Individual Retirement Account by April 15thand count it towards the previous year, you can’t do that with your company’s retirement plan. As a result, be sure you have funded your 401(k) or other plan as fully as possible by the end of the year. Remember that different kinds of plans have different contribution amounts with varying catch-up rules for older employees. Talk to your company’s human resources department to be sure you understand all of your available options.

You can do it!

Completing all of these tasks will help you end 2019 on a high note. However, I have one last piece of advice. Don’t let the holidays make you crazy. Keep your stress level low, and spend time doing things that you and your loved ones find meaningful. Review your cash flow, and don’t spend more money than you can afford. Starting 2020 without bills from the past holiday season is your first step toward a happy, prosperous New Year.

Meet Peggy

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.