This post may contain affiliate links. Full disclosure policy

THIS POST MAY CONTAIN REFERRAL LINKS. IF YOU CLICK THROUGH AND TAKE ACTION, I MAY BE COMPENSATED, AT NO ADDITIONAL COST TO YOU.

As I’ve mentioned, financial wisdom is about as exciting to me as tapioca pudding or reading a phone book.

But it’s just so important for a woman to have a handle on her finances, especially in the years beyond 50. This past year, my husband and I have put this at the top of our to do list.

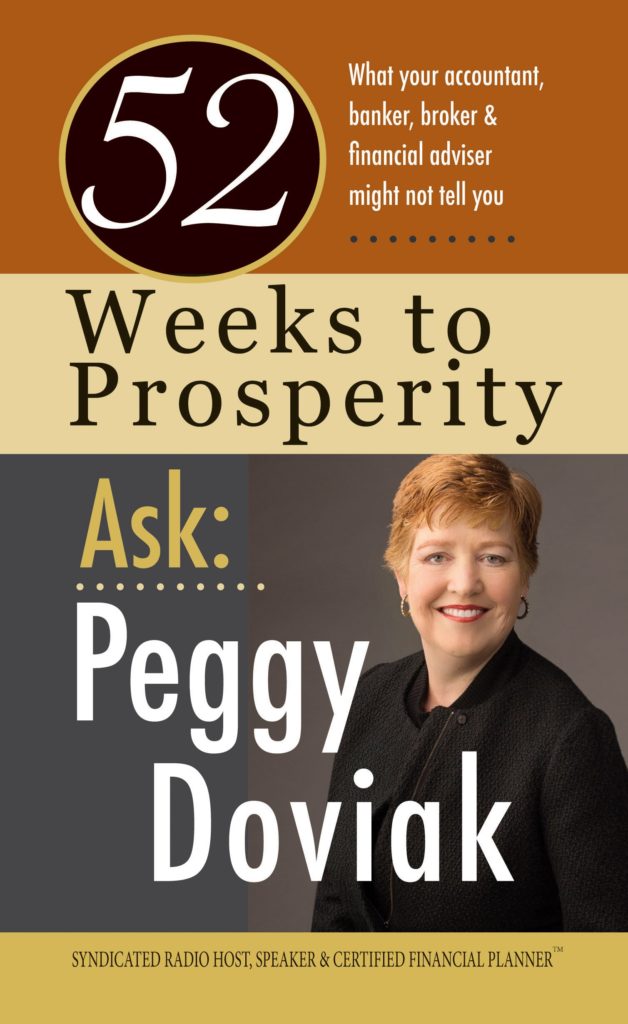

My search for financial wisdom promptly delivered me to the buy button on Amazon for Peggy Doviak’s 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You.

This book is awesome. It’s simple and easy to understand It offers actionable plans. It sets you up for success.

You probably remember Peggy showering us with wisdom in her recent posts about when we can afford to retire and how to curb holiday spending. These happen to be two of our most popular blogs on the site! And for good reason. They are just chocked full of nuggets of wisdom.

Financial Resolutions for 2019

The day after Christmas can be a little depressing. The last gift has been opened, the last Hallmark movie watched, and the cat finally has free rein over the Christmas tree. But don’t be sad. The holidays aren’t over yet. New Year’s Eve is only a week away with all the hope and promise of a brand-new beginning.

Are you making any New Year’s resolutions? If you are, do any of them involve your money? If so, you’re in good company. Common New Year’s resolutions include paying off debt and saving more. Unfortunately, our resolutions, money or otherwise, tend not to fare very well. In fact, 35% of us will have given up by the end of January. Most of the rest of us aren’t far behind.

Why are we so good at making resolutions and so bad at keeping them? I think it’s because we unknowingly set ourselves up for failure. I want to give you some tips to help you specifically with your financial New Year’s resolutions.

Changing the Conversation

First, change how you talk about your plan for 2019. Don’t say, “I’m not good at money, but I’m going to try to spend less this year.” Do you hear what you’re saying? “I can’t do it, but I’m going to try.” Don’t start your resolution by explaining why you won’t be able to succeed. Instead, clearly state that you are going to save money, and end your sentence there.

I think we run ourselves down for a couple of reasons. First, we provide our excuses at the same time we make our resolutions. That way, if we don’t succeed, we’ve already explained away the failure. But I believe there’s another reason, as well. Most of the time, our New Year’s resolutions are aspirational, and we honestly have no idea how to keep them.

But don’t despair—we can fix that. Let’s start by temporarily changing the terminology from “resolution” to “goal.” Good financial goals have three components. They are very specific, they have a dollar value associated with them, and they have a time horizon.

Set Yourself Up for Success

Here’s an example of an ineffective goal. “My plan for 2019 is to have plenty of money in retirement.” Sounds good, right? Who doesn’t want that? But here are the problems.

To begin, you don’t define when you want to retire. The steps you need to take are very different if you want to retire at 55 or at 70. Additionally, how much money is “plenty of money”? You will need to do some cash flow work to decide how much money you will need each month. Once you know your amount and your time horizon, you and your CFP® pro can determine how much you need to save each month to meet your goal. That amount of monthly savings then becomes your New Year’s resolution: “In 2019, I want to save (fill in your calculated amount) each month, so I can retire at age 65 with 90% of my current income.”

Doubling Down on Debt

Maybe your resolution is to pay down some debt. Again, this is a great idea, but you need to be specific. First, be sure that you are not incurring additional debt and if you are, try to get that under control. Next, look at your cash flow and decide how much money you can apply to your existing debt each month. Then, make that your New Year’s resolution: “In 2019, I won’t increase my current debt level, and I will lower it each month by the accrued interest plus $50.”

See how the two modified goals give you a specific game plan? Those are resolutions you can measure and know you have been successful!

It’s likely that you have more than one financial goal, so you might be considering several resolutions. Be careful if you decide to get overly ambitious. You already know you have limited financial resources, and you don’t want to stretch yourself too thin and set yourself up for failure. It’s possible that you will need to complete some goals first and then others later. Additionally, keeping your current financial situation reasonable carries major benefits.

Be Realistic

You need to maintain enough monthly cash flow to pay your obligations and bills and keep a little spending money, in addition to achieving your financial resolutions. It’s rarely a good idea to make a general proclamation like, “I will never eat out again,” or “I will shop with a list and never buy anything that I didn’t write down.” Although your statements sound good, they aren’t realistic. As soon as you decide you will only take your lunch to the office, you’ll get a call from a friend you haven’t seen in years. Your pal is in town for just one day, and she wants to have lunch with you.

I hope you say yes because staying in contact with old friends makes us prosperous. If you take your lunch the other four days that week, you will be much better off than you would if you ate out each day. However, if you have vowed never to eat out again, you may feel like a failure after lunch. That feeling may translate into extra spending at the grocery store that night on your way home from work. Or maybe you don’t bother making your lunch again that week. Your guilt for the original purchase tends to translate to more spending.

Be Kind to Yourself

To help you keep any financial goal, don’t beat yourself up if something goes wrong. Just put it behind you, and try again the next day.

Additionally, maintain a little spending money that you can use for anything you want. That way, you don’t go off track! The amount will be a directly related your financial situation.

Speaking of going off track, what happens when it’s May, and your New Year’s resolution is lying in a heap? Your plan sounded great back in January, and for a while, you saw a path to success. But now, summer is approaching, and you know you are so far behind that you couldn’t possibly get there. It’s okay; don’t give up. I want you to pretend that you are seven days from the beginning of the year. Use that time to review your information and revisit your resolutions.

Be Honest with Yourself

Be really honest with yourself. Why do you think you weren’t successful back in January? Maybe you stalled somewhere in the goal-planning process. Maybe your goal was just too much of a financial stretch. Or maybe life got in the way. It doesn’t matter. I’m not going to judge you, and I don’t want you to judge your partner or yourself. I want you to try again. If saving the amount you calculated was too difficult, then try to save half. If another goal with a higher priority has arisen, address that one, but still try to make some progress toward your original ideas. I know that this solution is not going to keep you on track for the path you calculated in January. But after talking to many individuals, I’ve learned something. When people feel overwhelmed, they don’t take any action at all. Even though you may not be saving as much as your plan recommended, you’re still moving in the right direction. You’re in better shape than you were last year. Half of financial success is just not giving up. You can do this. And your efforts will help make 2019 your best financial year ever!

About the Author

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.