This post may contain affiliate links. Full disclosure policy

THIS POST MAY CONTAIN REFERRAL LINKS. IF YOU CLICK THROUGH AND TAKE ACTION, I MAY BE COMPENSATED, AT NO ADDITIONAL COST TO YOU.

Have you noticed that here at FierceBeyond50, I post about all kinds of topics relevant to the beyond 50 lifestyle, everything from health and fashion, to downsizing and personal relationships, but not finances?

There’s a reason for that.

I suck at money. Big time.

When the conversation drifts toward topics of personal finance, one of two things happens. Either I start to feel very bored and very sleepy, or I experience the anxiety that can only be overcome by starting a new craft project.

Financial discussions confuse me and scare me. The first response tends to exacerbates the second response, I’ve noticed. The less I understand about money matters, the more frightening they become.

Even in my ignorance, I do understand that it’s important for a woman to have a handle on her finances, especially in the years beyond 50. That’s why, with a certain amount of trepidation, I’ve recently undertaken a personal quest to do exactly that.

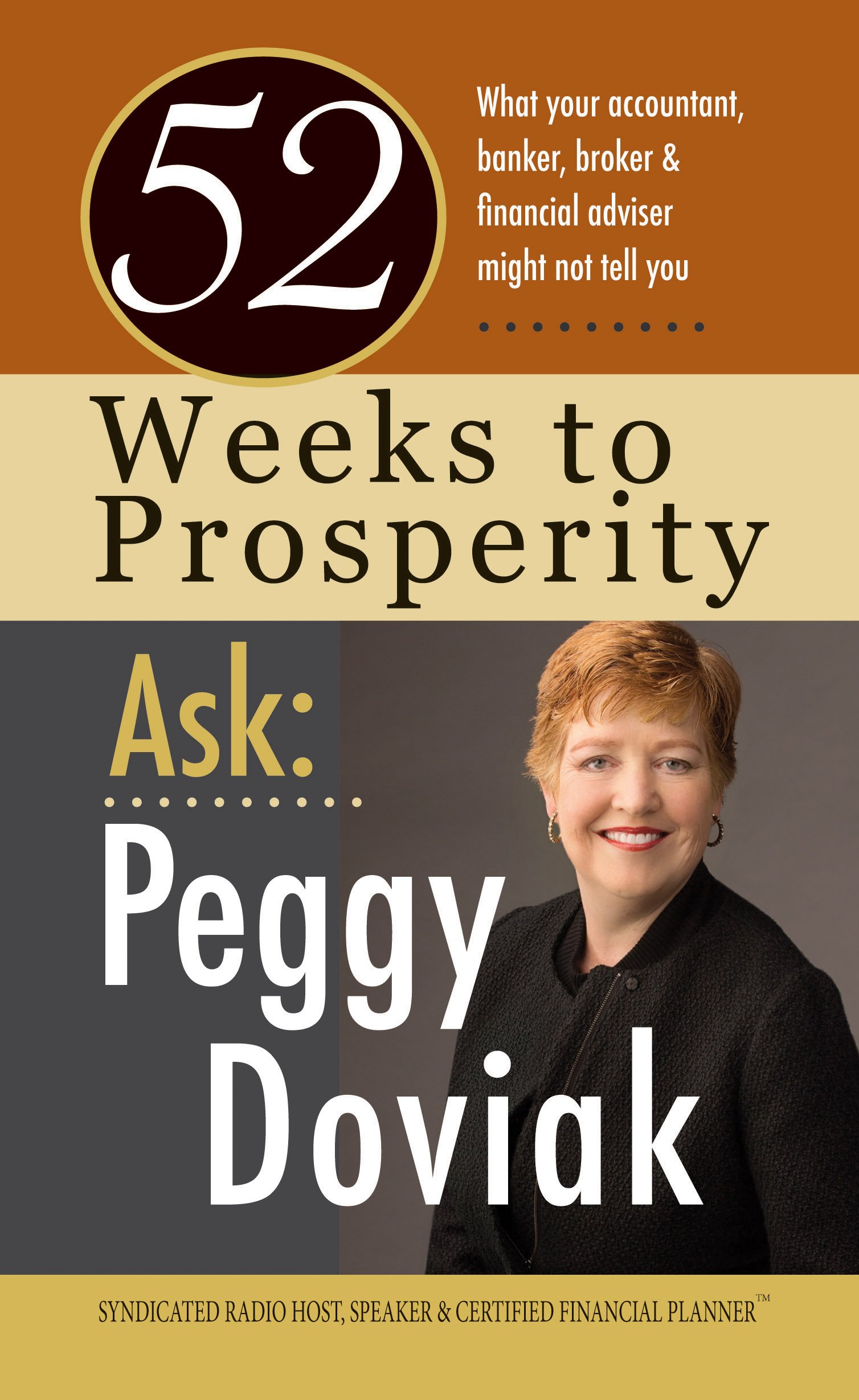

Not surprisingly, my search began with books. And, lucky for me, it soon brought me to the exact book I needed – 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You.

I highly recommend this book. It’s very clear and easy to understand and has specific action plans to help readers corral and steer their financial futures. If you know me at all, you know how I love a good action plan! Having a whole year to work through them seemed less intimidating, like something I could actually do. My husband and I are already working through some of these steps and it’s been an illuminating experience. (I’ll be blogging more about that in the future, so stay tuned.)

Something else I loved about this book was the warm, conversational tone of the author. Peggy Doviak seemed like somebody who would be easy to talk to, the kind of lady who I’d want to invite into my kitchen for a cup of coffee and a good gab.

Since Peggy lives in Oklahoma and I live in Oregon, a coffee date would be complicated. That’s why I decided to do the next best thing – invite her to guest blog. Actually it’s even better than a coffee date because I get to share her with all of you.

Today I’ve asked Peggy to write about a question that’s on the mind of so many Beyond50 readers – When can I retire?

Read on for Peggy’s answer to this very important question!

Are you terrified you can never retire? If so, you’re in good company. We’ve all seen the statistics about saving money in our twenties, and the young people who have committed to that strategy just rock! However, many of us did not plan for our retirement in our twenties, thirties, or sometimes even forties. We always had a “good” reason, but still, we didn’t save. Suddenly, OMG, we’re closing in on being 65! We need a solution, and we need it now.

Unfortunately, the financial services community understands our panic and, all too often, tries to exploit it. Over plates of cold chicken fettuccini and a never-ending PowerPoint, a local financial adviser tells us that if we haven’t saved a million dollars by now, we will be eating cat food during our twilight years. The adviser may also warn against counting on the viability of both Social Security and any pension we have earned. But never fear—he has the perfect product to meet our needs, whatever they are. Just sign here.

DON’T! Maybe the sales pitch really does offer an appropriate product, but don’t make your decision from a position of fear. When people are anxious or ashamed, they are desperate for a quick solution that provides peace of mind. When an investment product claims to offer financial certainty, it’s appealing. But remember—they bought you the fettuccini.

Instead, take time to find a CERTIFIED FINANCIAL PLANNERTMprofessional who embraces the fiduciary duty of acting in your best interest. She or he will look at your entire financial life and assist with some of the more complex calculations.

When Can I Retire? It Depends.

Even after you find a financial planner, you still need to take time to understand your money. You will be making many decisions about your financial goals and, probably, implementing a few course corrections. And you’ll start by gathering some data.

It’s impossible to create a retirement plan without first determining how much money you think you will spend each month. The easiest place to begin is by looking at what you are spending today. Do you know that amount? Honestly, many people don’t.

To avoid estimation errors, for thirty days, I want you to write down all your spending. Yes, all of it. Mortgages, utilities, cable, cell, eating out, groceries, entertainment—I want you to write it all down. Additionally, adjust for vacation spending, gifts, and events that create costs other times of the year.

At the end of the month, divide your purchases between expenses you must pay and the things you like to buy but could live without. Then, looking at the entire list, what expenses do you think you will pay during retirement? It’s likely some of them, like dry cleaning bills or a mortgage, will go down or be eliminated.

Running the Numbers

It’s also possible that you incur additional monthly costs. You’ve probably already considered expenses like healthcare, but don’t forget that you may need assistance mowing and cleaning, especially if your goal is to stay in your home. All these considerations should let you create a good estimate of the money you will spend each month during retirement.

The next set of calculations is much easier if you employ a CFP® pro. Your final goal is to know how much money you should save each month to meet your retirement need. The first step is to adjust your monthly spending for inflation. Then, any Social Security or pension benefits, will provide income to offset at least some of that spending. After that, use a reasonable growth and inflation rate to calculate the total amount of additional money necessary to fund your retirement expenses. Finally, that number is used to calculate your additional monthly savings rate.

*Gasp for a breath.* See why I want you to use a financial planner? The formula can be overwhelming, and your results need to be correct.

Evaluating your Position

Once you know how much you need to save, you’re in one of three places. Maybe, you have already begun to save enough money, and all you need to do is stay on track. Alternatively, your savings rate is close to adequate, but not quite there. Or finally, oh wow, you’re not even close!

If your retirement savings is close but still a little short, you might be inclined to take more risk in your investments to earn a higher potential rate of return. If you initially chose a very conservative strategy, this solution might work. But if you are already making aggressive or even moderate return assumptions, it’s risky to assume you can earn one or two more percent each year. Remember that the long-term rate of return for stocks is 11%. Moderate portfolios (50% stocks/50% bonds) are historically more likely to provide an average return of 8%.

Since raising your return assumptions always increases the risk of the portfolio, you might be better served to look back at your spending assumptions. Could you make any modifications there? Additionally, you might find that delaying retirement or Social Security benefits a year or two might make a big difference.

60 is the New 40

But what do you do if your retirement need seems impossible to achieve? First, don’t panic. The easiest way to improve your financial situation is to plan to work longer. By working additional years, you have an opportunity to save more, and you do not use existing retirement resources as early.

I know you want to retire, but 65 isn’t what it used to be. Popular magazines tell us that 60 is the new 40. Even if that seems suspect, when Social Security began paying benefits at 65, the average life expectancy was 61 years old! Today, average life expectancy has increased to 75. Add good nutrition, physical safety, and proper medical care, and most of us expect to live much longer than that. 60 might not be the new 40, but it also isn’t the age our productive lives end.

If you continue to work, you can delay taking Social Security. Each year you defer taking your benefit after age 62 lets it grow by 8% until the amount maxes when you are 70. That’s a respectable rate of return!

Some people express concern over delaying Social Security because they are afraid of its financial viability. The easiest solution to this issue would be by making more income subject to the tax. Additionally, senior citizens would storm Washington, DC, and I think no lawmakers want those optics!

Consider a Career Change

If you can’t afford to retire yet, remember that continuing to work does not mean you must stay in your current job. This is your opportunity to do something new with the last third of your life! Maybe you want to stay where you are, and maybe you want to pursue a new venture. Additionally, you might be able to offset your retirement need simply working part time rather than full time.

If you want to branch out as an entrepreneur, take some time while you are still earning an income to complete a business plan, determine the costs and earning potential, and maybe even run both your current position and your new endeavor at the same time. Small businesses have a notoriously high failure rate, so be very careful.

A better option might be to find a position in an established business that you find interesting. This path gives you the opportunity to branch out without the risks involved in opening a business. It’s the best of both worlds.

So you can absolutely plan for a fulfilling retirement, even if you started late. With a little effort, you can buy your own fettuccine and a nice bottle of wine to go with it!

About the Author

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.

CERTIFIED FINANCIAL PLANNERTMpractitioner, Peggy Doviak, knows how stressful money can be. Her fifteen years as a financial planner and a national speaker to both financial professionals and consumers have convinced her that most people fear their money. That’s why she wrote 52 Weeks to Prosperity – Ask Peggy Doviak: What Your Accountant, Banker, Broker & Financial Adviser Might Not Tell You. In it, she addresses 52 financial planning topics to enable individuals to become comfortable with the vocabulary and issues of their financial lives, so they can participate in the planning process with a professional. Learn more about Peggy on her website, www.peggydoviak.com.